In recent years, the EU's economic and trade policies towards China have become increasingly strict. Especially recently, the EU and its major member states have implemented numerous restrictive measures regarding Sino-EU economic and trade relations. These measures include attempts to introduce discriminatory regulatory laws targeting China, such as the Cybersecurity Act and the Industrial Accelerator Act. The EU has even proposed a package of measures and the signing of a new "Plaza Agreement" with China in order to address the EU's deficit with China.

Undoubtedly, these measures and suggestions will have a serious impact on the normal economic and trade relations between China and Europe. How did the economic and trade frictions between China and Europe arise? Why does the European Union take an increasingly strict stance on economic and trade relations with China? What is the underlying reason behind this, and how will the economic and trade relations between China and Europe develop in the future? This article attempts to provide answers to these questions.

In recent years, the EU's economic and trade policies towards China have continued to tighten. Various trade investigations, restrictive laws, and technical controls have been implemented. These measures are all related to two core accusations of the EU against China: the so-called "trade imbalance" and "supply chain security."

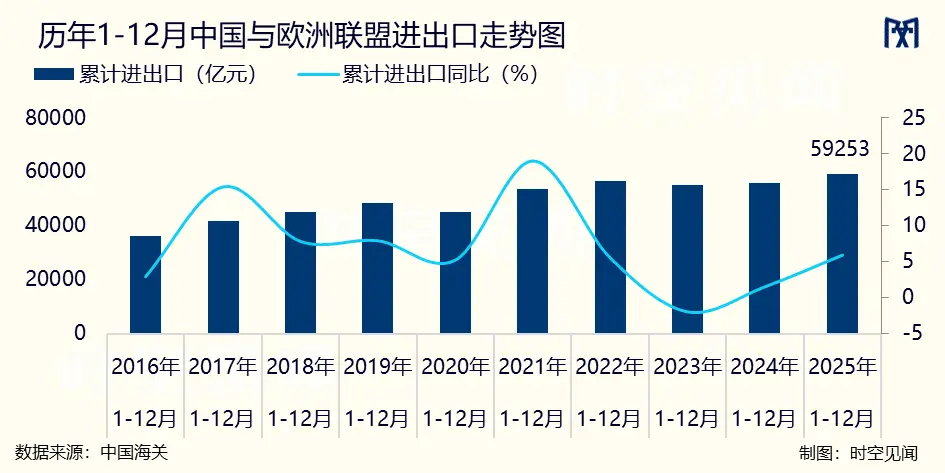

In terms of trade “disbalances,” at the beginning of this century, China became deeply integrated into the global industrial chain. There has been a long-term trade surplus for Chinese goods with Europe, especially in the past five years, when the trade deficit remained high (ranging from about 2000 to 4000 billion euros). The EU believes that ongoing deficits with China harm the development of European industries. Unequal market access, industrial subsidies, and excess production capacity in China are considered the core causes of trade imbalances. Based on this understanding, the EU has successively launched countervailing investigations on electric vehicles, trade remedies on steel and photovoltaic products, introduced the “Foreign Subsidy Regulations,” established review mechanisms for industrial subsidies from various countries, and brought a large number of China’s advantageous manufacturing industries under regulatory oversight.

In terms of supply chain security, under the backdrop of the Russia-Ukraine conflict, the EU believes that economic interdependence is no longer a bond that stabilizes relations between Europe and China. Instead, it has been “armed” and becomes a source of strategic vulnerability. The excessive reliance on China for strategic materials such as critical minerals, new energy equipment, 5G communication devices, and photovoltaic components will put Europe in a vulnerable and even dangerous position.

Based on this, the EU has introduced a systematic 'risk reduction' policy package. In the tech sector, restrictions have been imposed on Chinese companies like Huawei to participate in EU 5G infrastructure projects. At the legislative level, initiatives such as the 'Net Zero Industry Act' and the 'Industrial Accelerator Act' are being implemented or advanced. The EU supports domestic companies through subsidies for local industries and setting import barriers, thereby reducing its dependence on imports from China in key areas. On the diplomatic front, the 'Global Gateway' initiative is being promoted. Infrastructure and industrial chains are being laid out in Central Europe, Africa, and Southeast Asia, aiming to establish alternative supply chains that do not rely on China.

Regarding issues such as trade imbalance and industrial chain security, the Chinese and European sides have completely different, even opposite, understandings. From a European perspective, the responsibility for the trade imbalance lies with China. Firstly, it is due to large-scale industrial subsidies. The EU believes that governments have reduced the production costs of products such as new energy, photovoltaics, and electric vehicles through fiscal support, creating an unfair price advantage. Secondly, there is the so-called undervaluation of the RMB, which artificially reduces the cost of export goods and enhances export competitiveness. Thirdly, there is a lack of domestic demand in China's consumer market, making it difficult to absorb large industrial production capacities. As a result, a large amount of "overcapacity" products are dumped into the international market.

Under this logic, Europe considers itself in a passive and disadvantaged position. The tariffs, trade investigations, and restrictive regulatory measures it implements are essentially reasonable measures to correct market distortions and maintain a fair competitive order globally. They are also necessary means to protect domestic industries and safeguard European economic security.

However, from a Chinese perspective, China's trade surplus is not due to subsidies or so-called 'overcapacity', but rather because of China's higher international competitiveness compared to Europe. It is also an objective result of the international division of labor and structural industrial differences under the backdrop of globalization, and there is no artificial distortion or intentional manipulation. The following factors are the fundamental reasons for China's trade surplus with Europe:

Firstly, China possesses the most complete industrial chain system in the world. From the processing of raw materials at the upstream, the manufacturing of components at the midstream, to the assembly of finished products at the downstream, complete industrial clusters significantly reduce production, logistics, and supporting costs, creating a natural cost advantage. This is a core competitiveness that has been developed over decades of industrialization, infrastructure construction, and large-scale industrial workers, and it is not the result of isolated policy subsidies alone.

Secondly, China's status as a global manufacturing center. Currently, Chinese manufacturing accounts for about 30% of the world's production capacity. As European industries shift overseas, local manufacturing becomes relatively hollowed out, naturally creating a demand for imports from China. This situation is also beneficial to many Western countries. Therefore, China's trade surplus to Europe is an objective result of global division of labor.

Third, continuous technological innovation and industrial upgrading continuously strengthen export advantages. In recent years, China has achieved technical autonomy breakthroughs in new energy, photovoltaic, energy storage, and battery fields, forming product competitiveness through technology iteration and gaining global market favor by price-performance ratio. This is a normal result of market competition. In fact, Europe's existing problems have reduced its competitiveness, which has been admitted by the EU's "Draghi report." It is precisely this kind of competitiveness boost/decrease that has become a major cause of EU disadvantage.

Currently, the measures taken by the European Union against China manifest as a strong protectionist policy towards domestic markets. From the perspective of the European Union, the short-term goal of protectionism towards China is to strongly protect domestic industries and alleviate the pressures of industrial hollowing out and slow economic development.

Europe is currently facing multiple internal economic difficulties, due to factors that are not limited to the following: First, energy shortages. After the Russia-Ukraine conflict, prices of natural gas and electricity in Europe have risen significantly, leading to soaring manufacturing production costs. This has caused a significant decline in the competitiveness of local new energy and traditional manufacturing industries. Second, innovation challenges. Europe has serious deficiencies in investing in innovation in high-tech fields. Its inherent advantages in advanced technologies are being continuously surpassed by external competitors, making it difficult to escape the "middle-tech trap." This results in a heavy reliance on traditional manufacturing industries, making industrial transformation challenging. Third, population aging and persistent labor shortages mean that labor costs remain high for a long time. Fourth, overly stringent environmental and labor regulations increase the operating costs of local businesses and hinder the formation of competitive multinational corporations in high-tech fields. And so on.

Facing these various problems, Europe is completely unable to resolve them in the short term. It can only use trade barriers and industrial support policies to counter the competition from Chinese products, delay the decline of domestic industries, preserve jobs in the local manufacturing sector, and alleviate the protests from domestic industry groups and unions. This also becomes the simplest way for the EU to appease internal public opinion, deal with the challenges of 'political polarization', and resolve domestic economic contradictions.

The short- to medium-term goals of protectionism are aimed at curbing China's industrial upgrading and maintaining Europe's inherent dominant position in the global industry. Over the past few decades, Europe has relied on high-end manufacturing, precision equipment, biomedicine, and upstream technologies in new energy to occupy the top of the global value chain. It has long enjoyed excess profits in the global industrial chain through technology, standards, and patents. However, with China's industrial transformation and upgrading, China has achieved leapfrog development in high-end manufacturing fields such as new energy, electric vehicles, photovoltaics, energy storage, and artificial intelligence, directly challenging Europe's traditional advantages. In this context, the EU has introduced a series of restrictive policies, attempting to curb China's growth in high-end manufacturing and slow down the pace of industrial upgrading, while maintaining its dominance in global high-end industries and technology standards. Representative regulatory measures include the "Industrial Accelerator Act," "Net-Zero Industry Act," "Cybersecurity Act," and "Foreign Subsidies Regulations," which aim to disrupt the current Sino-EU economic and trade competition pattern and reshape Sino-European economic and trade relations, thereby maintaining Europe's long-term industrial advantage.

Trade frictions and their underlying purposes are the result of multiple underlying logics working together. These logics manifest as differences in interests, beliefs, strategic choices, and systems.

Among these, the gap in interests is one of the fundamental reasons that led the EU to take restrictive measures against China. In the past, there was a vertical division of labor and mutual complementarity between China and Europe. Europe provided high-end technology, capital, and advanced components, while China was responsible for processing and assembling products as well as low-end manufacturing. Now, China has completed the upgrading of its entire industrial chain. Both sides are competing on levels such as new energy, high-end equipment, and digital industries. The original complementary division of labor is gradually disappearing, and competition is becoming increasingly intense.

The second logic is the concept gap. Europe wishes to maintain the old global economic order dominated by the West, where Europe and America hold the power to set rules. They rely on long-standing international trade rules, technical standards, and financial system governance to create an economic order characterized by “Western dominance and developing countries’ dependence,” thereby securing high monopoly profits. However, China advocates a new type of global economic order based on sovereign equality and mutual benefit and win-win outcomes. China believes that all countries should have the right to independently choose their industrial development policies and opposes interference in other countries’ economic development using a single standard. This is the conflict between Europe’s hierarchical view of order and China’s view of an equal order.

The third level of logic involves the strategic differences between security generalization and globalization. Under the guidance of macro-strategic thinking in geopolitical competition, Europe adheres to the principle of ‘security first’. It secures economic issues and forcibly intervenes in Sino-European economic exchanges through political means. In contrast, China supports globalization, believing that deep economic integration among countries is an important link for stabilizing international relations and resolving geopolitical conflicts. China opposes weaponizing or generalizing economic and trade tools as means of security, resulting in two different development strategic concepts.

The fourth layer of logic is the institutional gap. There are fundamental differences in institutions between China and Europe. China follows a socialist market economy system, while Europe operates under a capitalist market economy system. There are natural distinctions between the two sides in terms of economic development models, how government and markets are managed, and industrial regulation. The EU uses its own institutional standards as a benchmark, defining China’s industrial support policies as “market distortion,” thereby exacerbating the economic and trade differences between the two sides and becoming one of the inherent causes of economic and trade tensions between them.

Facing the continuous tightening of restrictive economic and trade policies towards China by the EU, China should adopt a layered approach. It is necessary to distinguish between compliance measures and discriminatory barriers. At the same time, China should improve policy tools and expand diverse cooperation opportunities to mitigate the pressure exerted by the EU.

First, efforts should be made to establish a layered response mechanism, with differentiated handling of various EU regulatory policies. For tariffs, trade investigations, special restrictive laws, and measures that violate WTO rules or other international trade regulations, which involve clear national discrimination, harm China’s core industrial interests, or even undermine China’s sovereignty rights and interests, countermeasures can be taken in accordance with WTO rules. These countermeasures can be pursued through legal channels to protect the legitimate rights and interests of domestic industries. However, for EU policies that comply with international common rules, have universality, and are non-discriminatory in terms of industrial regulation, environmental protection, and labor standards, Chinese enterprises can actively align themselves with international rules, adjust industrial norms, reduce friction points, avoid full-scale confrontation, and moderately deepen economic and trade cooperation with the EU.

Secondly, continuously improve domestic economic and trade countermeasures and mechanisms for safeguarding interests. Strengthen the legal framework for foreign trade relief and industrial security inspections. Expand measures such as tariffs, trade barriers, and investment reviews to form a comprehensive set of policy tools. To prevent the outflow of core industries and the leakage of core technologies, gradually introduce and implement the "Foreign Investment Law" based on regulations such as the "State Council's Provisions on Foreign Investment." Regulate enterprises' foreign investment activities and establish mechanisms for reviewing the transfer of core technologies and key industrial chains abroad. Prevent the excessive transfer of core technologies and production capacity of strategic industries such as new energy, semiconductors, and high-end equipment overseas, thereby safeguarding the foundation of domestic manufacturing industries. At the same time, align with WTO rules to optimize domestic industrial support policies, reduce the pretexts used by the EU for trade investigations regarding "subsidies," and enhance the international compliance of China's industrial policies.

Third, adhere to compliant operations and explore further opportunities for bilateral cooperation. Although the EU has introduced several regulations that may be considered discriminatory, unlike the US’s “one-size-fits-all” approach to tariffs, there is still room for China’s economic and trade cooperation with the EU. Therefore, domestic companies expanding overseas should comply with EU laws and regulations, carbon tariffs, industry standards, and foreign investment review rules. By doing so, they can reduce the risk of trade tensions, stabilize existing investments and market share in Europe, and use topics such as green energy, low-carbon technologies, and circular economy to offset industrial competition. Practical cooperation can also dilute the confrontational atmosphere resulting from geopolitical negotiations. Of course, all compliant actions should be conducted with the aim of maximizing profits, and must not undermine China’s sovereignty and core interests.

Fourth, explore third-party markets and reshape a diversified economic and trade layout. Relying on the free trade area networks between China and Europe, establish new industrial cooperation channels in third-party markets such as Southeast Asia, the Middle East, Latin America, and Central Asia. Promote “agency globalization” – a economic exchange model where direct economic and trade exchanges between major economies are replaced by indirect connections through third parties, thereby reducing competition and conflicts in the direct market competition between China and Europe. At the same time, deepen economic and trade relations between China and EU member states, as well as with local provinces and cities at multiple levels. Differentiate between the overall policies of the EU and the differentiated demands of individual countries. Take advantage of some European countries’ emphasis on the Chinese market and their opposition to complete disconnection from China, to expand economic and trade buffer spaces with Europe.

Based on the above analysis, future economic and trade relations between China and Europe may become more complex than today. The EU's restrictive economic barriers against China will become stronger and more systematic. However, deep cooperation between both sides is indispensable. ‘Detaching and cutting off ties’ is not an option for either side.

First, the EU’s various restrictive regulatory rules towards China will become more common. Economic and trade disputes will not disappear in the foreseeable future, and may even increase. Due to considerations of industrial protection and geopolitical competition, the EU will continue to introduce regulatory measures targeting China. Trade remedy investigations, foreign investment safety reviews, and controls on technology exports are likely to increase, leading to long-term industrial competition disputes. However, it is difficult for the EU to completely cut off economic and trade ties with China. European companies have significant market interests in China, and complete deconnection would severely impact European exports, product competitiveness, consumer and inflation stability. Moreover, the need for cooperation at the international governance level forces both sides to reduce trade frictions in order to maintain basic mutual trust. Therefore, economic and trade disputes and cooperation with China will coexist for a long time.

Secondly, greenfield investments in Europe have become a new growth point in the bilateral economic and trade relations. Due to the increased export barriers and various restrictions on mergers and acquisitions, some Chinese enterprises exporting to Europe will have to increase their greenfield investments in non-strategic areas within Europe in order to avoid EU regulations. However, the EU’s requirements regarding equity restrictions, localization, and transfer of advanced technology for Chinese enterprises, as well as security checks, may limit China’s confidence in greenfield investments in Europe.

Third, competition in technology and standards could become a new focus of negotiation. The traditional trade disputes between the two sides will gradually expand to include competition in high-tech industries, industry standards, carbon regulations, and digital governance. The EU will try to continue leading global green and digital trade rules by relying on its mature industry standards. However, China will accelerate the internationalization of its own standards. The standard negotiations between the two sides in areas such as new energy, artificial intelligence, and carbon tariffs are expected to intensify.

Fourth, third-party markets have become a new factor in shaping relations between China and Europe. On one hand, both sides are seeking to reduce their dependence on each other’s single markets and continue to expand their ties with markets in ASEAN, the Middle East, Latin America, and Africa. The European Union is actively promoting negotiations and the establishment of free trade areas with these regions, laying out a “global gateway” strategy, and seeking key partners in critical minerals in order to engage in geopolitical competition with China. On the other hand, third-party countries such as Vietnam, Indonesia, Thailand, and Tunisia are becoming important “agent states” in reconnecting China-Europe supply chains. They are becoming crucial forces in shaping “agent globalization” between China and Europe, as well as in reshaping economic and trade relations between the two regions.